Monday, February 14, 2022

Please

find below our latest Weekly Trend Report covering major asset

classes and currencies.

Have

a nice week ahead.

Marc

Bentin

The major events of the past week were inflation

(US CPI) running hotter than expected with a 0.6% monthly gain which boosted yoy

US inflation to a 40 year high at 7.5%.

This initiated a raft of damage control comments

from Federal Reserve Officials claiming monetary tightening and tapering should

occur sooner and faster than expected with speculation building of a 50bps rate

hike in March with accompanying calls for an immediate halt of Federal Reserve

asset purchases…Rate hike “speculation” rose to 6.3 times a 25bps hike before

the end of the year.

Then on Thursday and Friday came a swift

deterioration on the situation in Ukraine as the US administration raised the

alert level, calling back diplomatic staff from Ukraine (including some military

personnel), urging its nationals to leave Ukraine immediately, as it claimed

Russia would soon (before the end of the Olympics games) move into Ukraine.

This triggered a massive risk off session on Friday

that erased the squeezy gains of the first half of the week, at the same time cutting

most of the bond market loss that the inflation surprise and accompanying Fed officials’

declarations had triggered.

While the so-called ECB pivot from the previous

week (when ECB President C. Lagarde hinted at the possibility of a rate hike

before year end following disappointing German and pan European CPI) triggered

some rise in core yields and peripheral spreads (Italian and Greek yields climbed

by respectively 20bps and 40bps, early last week, Friday’s “risk off” session

and some push back/ backpedalling from the ECB President who insisted that a

precipitous rate hike would not help resorb prices pressures related to the energy

crisis and supply bottlenecks, reduced those losses.

Friday’s biggest casualty were the Russian stock

market (-5%) and RUB (-2%) while US Treasuries rallied. With inflation at 7.5%, “talks” about the need

of an immediate rate hike of 100bps managed to reverse much of last week’s

losses, with 10-year yields trading back at 1.94% (after hitting 2.04% intraday

on Friday). WTI which had corrected slightly earlier in the week, also stormed back,

closing 4.5% higher on Friday.

Russia blamed the White House for conducting a mass

disinformation campaign against Russia while the White House said it was just

“trying to stop a war”.

The technical deterioration inflicted on Friday was

severe, including and starting with the underperformance of US citadels which fuelled

US indices last year despite 50% of the Nasdaq undergoing a severe correction

over the same period. Amazon, Tesla, Netflix, Facebook, Nvidia and recent IPO’s

all suffered a near 4% loss on Friday. GOOG dropped 3.25% while semis shed

-7.9%. There was continued deterioration in credit markets as well with traders

bidding up the price of protection on corporate bonds and high yields in

particular.

Also on Friday, University of Michigan US consumer expectations were

reported to have unexpectedly dropped to a fresh decade low (to 61.7 from 67.2 and 67

expected) with both current and expected conditions dropping and 12month inflation

expectations rising once more (to 5%).

All of the above being said, over the week end, Goldman and BoA reminded that while 2021 logged more

equity inflows ($913bn), than the prior 25 years combined, 2022 is on pace to

exceed this number by 45%”. While the risk of war and tapering are powerful deterrents

near term (as could be a recession) and while most of this year’s equity flows

are wrong footed, it remains nonetheless that FOMO will calculate in days,

weeks, months rather than years when the bottom is reached, especially, as is

likely, if the Fed (ECB, BoJ) remain (very) unlikely to deliver a “Volcker” moment

or anything of that nature.

Elsewhere in China last week, January aggregate

financing data came in 15% stronger than expected at USD972bn and trouncing a

previous record growth dating from January last year as the PBOC reiterated on

Friday it was encouraging banks to expand lending to bolster a slowing economy.

Stress remained visible among leveraged real estate developers and real estate

transactions dropped sharply over the past few weeks.

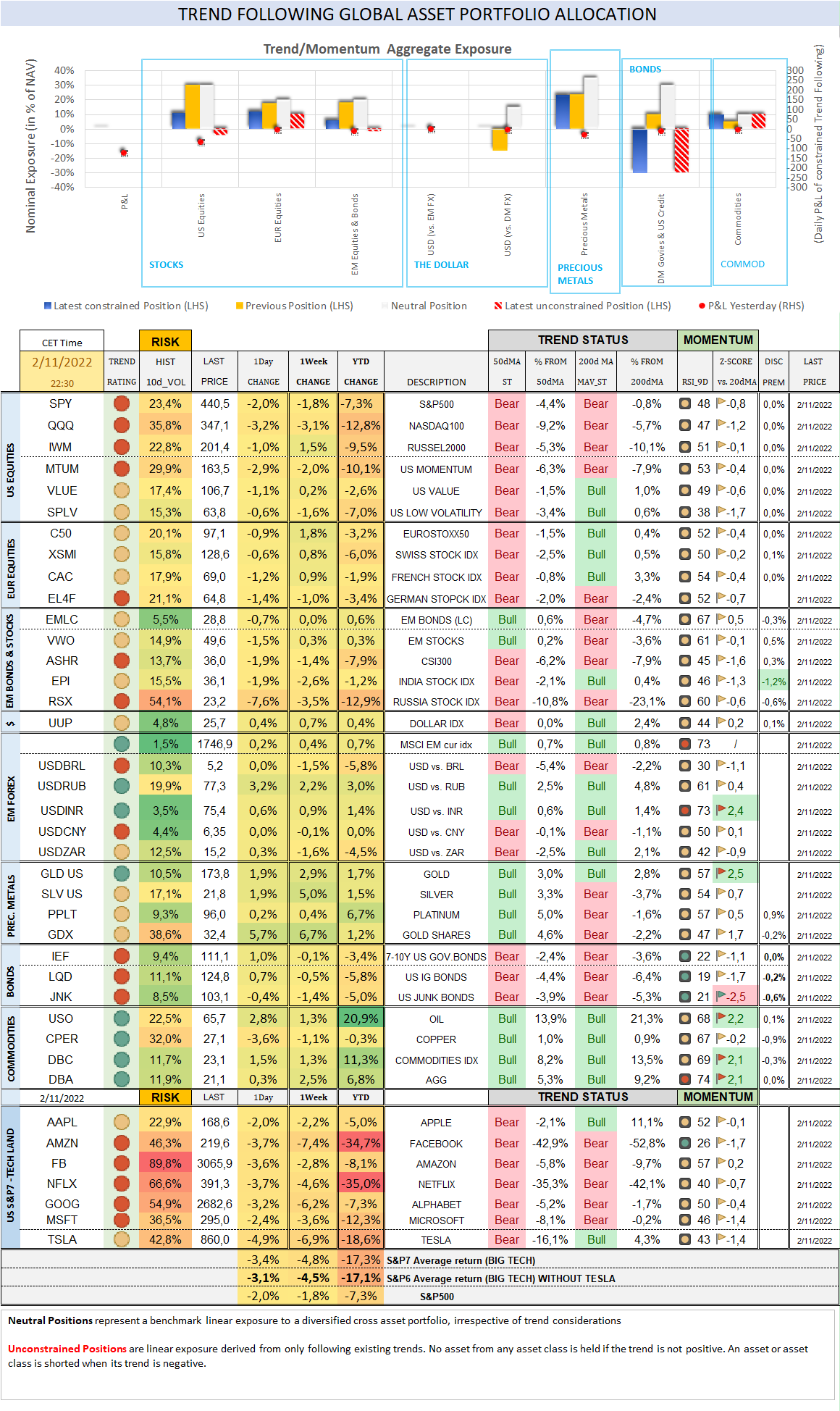

Over the past week, the S&P500 dropped -1,8%

(-7,3% YTD) while the Nasdaq100 sold off by -3,1% (-12,8% YTD). The US small

cap index gained 1,5% (-9,5% YTD).

Cboe Volatility Index rallied 19,7% (61,4% YTD) to

27,57.

With Friday’s move, every major US index and every

sector of the S&P500 now stand in “bear trend” territory (trading below

their respective 50d and 200d ma) with the exception of banking, energy (+27%

ytd) and metals mining (+8.1% ytd). The worst performance year to date comes

from semis (-18.5%), home building (-17.6%) and Biotech (-16.66%).

Last week, the Eurostoxx50 gained 1,8% (-3,2%),

outperforming the S&P500 by 3,7%.

Diversified EM equities (VWO) gained 0,3% (0,3%),

outperforming the S&P500 by 2,1%.

The Dollar DXY Index (UUP) measuring the USD

performance vs. other G7 currencies gained 0,7% (0,4%) while the MSCI EM

currency index (measuring the performance of EM currencies vs. the USD) gained

0,4% (0,7%).

10Y US Treasuries dropped 1bps (40bps) to 1,91%.

10Y Bunds climbed 9bps (47bps) to 0,30%. 10Y Italian BTPs underperformed rising

21bps (78bps) to 1,95%, underperforming Bunds by 5bps.

US High Yield (HY) Average Spread over Treasuries

climbed 2bps (52bps) to 3,35%. US Investment Grade Average OAS climbed 1bps

(17bps) to 1,17%.

In European credit markets, EUR 5Y Senior Financial

Spread climbed 3bps (20bps) to 0,75%.

Gold

rallied 3,0% (1,9%, Z-score 2,2) while Silver rallied 5,1% (1,5%). Major Gold Mines

(GDX) rallied 6,7% (1,2%), delivering the best daily performance of our score

card on Friday.

Goldman Sachs Commodity Index dropped -0,3%

(14,4%). WTI Crude gained

1,6% (24,7%, Z-score 2,2). J. Currie, the closely watched commodities

research head of Goldman opined last week that in 30 years in the business, he

has never seen commodity markets pricing in the shortages they are now. “We are

out of everything”, he said, pointing out that futures curves in several

markets are trading in super backwardation as traders keep paying up large premium

for immediate supply.

Overnight in Asia…

Ø S&P500 future +12 points; Nikkei -2.1%; CSI300

-0.6%

Ø Over the week end, L. Summers called for the Fed to

hold an emergency meeting to conclude QE early.

Ø On Thursday, just prior to traders hitting off for

a long week end, the BoJ announced a fixed rate operation to buy an infinite

amount 10-year notes at 0.25% today as 10-year yields approached this upside limit

of their yield anchoring extreme monetary policy. Nobody showed up this morning

to sell at 0.25% bonds trading at 0.21%

Ø A call between J. Biden and V. Putin over the week

end was inconclusive.

Ø During their Sunday phone call Ukraine's President

Zelensky asked US President J. Biden to visit Kiev in person amid pressing White

House claims that a Russian invasion is set to happen "any day" now. Russian Foreign Minister Lavrov tweeted over the week

end “After Russian troops finish drills and return to barracks, West will

declare 'diplomatic victory' by having 'secured' Russian 'de-escalation'.

Predictable scenario and cheap domestic political points.”

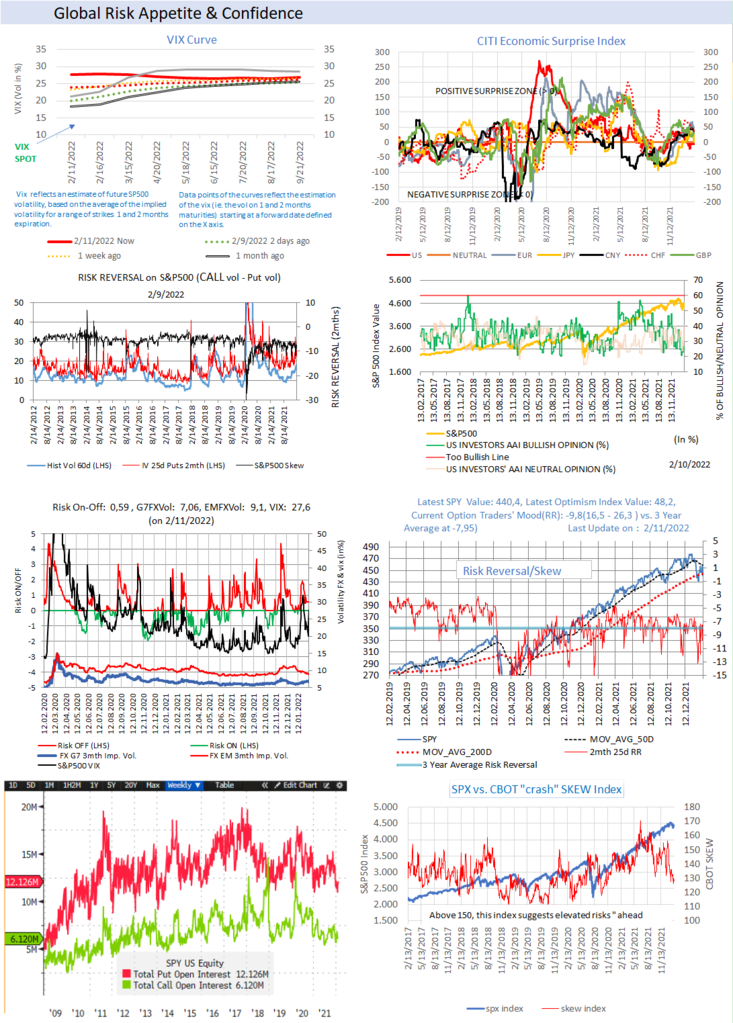

10 Days In Charts…

{kind=link}

Global

Risk Appetite & Confidence

Check out different gauges of Risk Appetite .

{kind=link}

Check China … (Stock

Indices, CNY…and Evergrande)

{kind=link}

Why Trend Following Matters and How It Can Help

You?

A disciplined and rule-based trend following investment

approach can serve as an effective portfolio insurance technique.

To receive a Daily Trend Status Update and round the

clock market and economic instant notifications, join the free trial for our premium research. No credit card needed.

To learn more about our premium research:

https://www.bentinpartners.ch/research

To join our free trial and choose your delivery preferences:

https://www.bentinpartners.ch/subscribe

Our Portfolio

Management and Advisory Services

Zero and sub-zero

interest rates are here to stay. As a private individual, a pension fund or a

foundation, we all share the same challenge!

To see how we can help

you secure your financial independence over the long term, meet your

obligations and mitigate tail risks,

Check our Pitch

and our FAQ’s.

BentinPartner GmbH is

an registered Swiss Financial Adviser

delivering professional portfolio management and research.

Please visit our web site or call us at

+41615444310. We’d love to hear from you and see how we can further assist you.

Join us on Linked In

To be removed from the

list, please send us an email by clicking here, mentioning “unsubscribe”

in the title.

To ensure that our emails

reach your inbox and not your spam folder, please consider adding

Marc.Bentin@BentinPartner.ch, Marc.Bentin@BentinPartners.ch and our alternate

address Bentinpartner@gmail.com to your safe address book. If you are using

Microsoft Outlook, simply right click on our email address, choose "add to

Outlook contacts" and then "save".

Important Disclaimer

© Copyright by BentinPartner llc. This communication is provided for information

purposes only and for the recipient's sole use. Please do not forward it

without prior authorization. It is not intended as a recommendation, an offer

or solicitation for the purchase or sale of any security or underlying asset

referenced herein or investment advice. Investors should seek financial advice regarding

the suitability of any investment strategy based on their objectives, financial

situation, investment horizon and particular needs. This report does not

include information tailored to any particular investor. It has been prepared

without any regard to the specific investment objectives, financial situation

or particular needs of any person who receives this report. Accordingly,

the opinions discussed in this Report may not be suitable for all

investors. You should not consider any of the content in this report as legal,

tax or financial advice. The data and analysis contained herein are provided "as

is" and without warranty of any kind. BentinPartner llc, its employees, or

any third party shall not have any liability for any loss sustained by anyone

who has relied on the information contained in any publication published by

BentinPartner llc. The content and views expressed in this report represents

the opinions of Marc Bentin and should not be construed as guarantee

of performance with respect to any referenced sector. We remind you that past

performance is not necessarily indicative of future results. Although BentinPartner llc

believes the information and content included in this report have

been obtained from sources considered reliable, no representation or

warranty, express or implied, is provided in relation to the accuracy,

completeness or reliability of such information. This Report is also not

intended to be a complete statement

or summary of the industries, markets or developments referred to in the

Report.

#fx #forex #investing #markets #riskmanagement #bankingindustry

#finances #money #traders #quants